Efficiency Before Fuel: Energy Savings as the Primary Decarbonisation Lever in Shipping

Why over 90% of the global fleet is ignoring the green transition potential already on board

Shipping is debating which green fuel will save it, while burning through regulatory penalties every day on ships that could already consume 15 to 25 percent less. Efficiency is not the stepping stone to decarbonisation. It is its primary, immediately available, and economically superior lever, and most decision-makers treat it like a footnote.

Executive Summary

Over 90% of the global fleet operates on conventional fuels; IMO CII targets require a 21.5% reduction in CO₂ intensity by 2030 versus 2019, while EU ETS and FuelEU Maritime costs escalate from 2026 onwards.

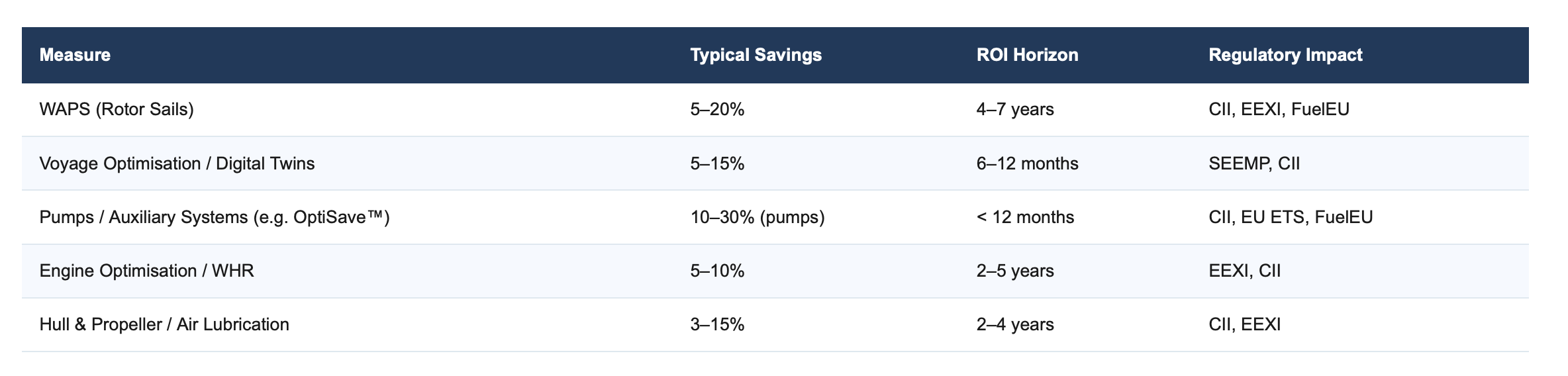

Wind-Assisted Propulsion, digital voyage optimisation and smart pump management deliver a combined 15 to 30% savings with payback periods as short as 12 months, using technologies that are available today and regulatorily recognised.

The maritime energy efficiency market is growing at an 11% CAGR to reach USD 3.39 billion by 2030; fleets investing now in combination solutions secure lower OPEX, stronger charter rates and regulatory resilience through 2031.

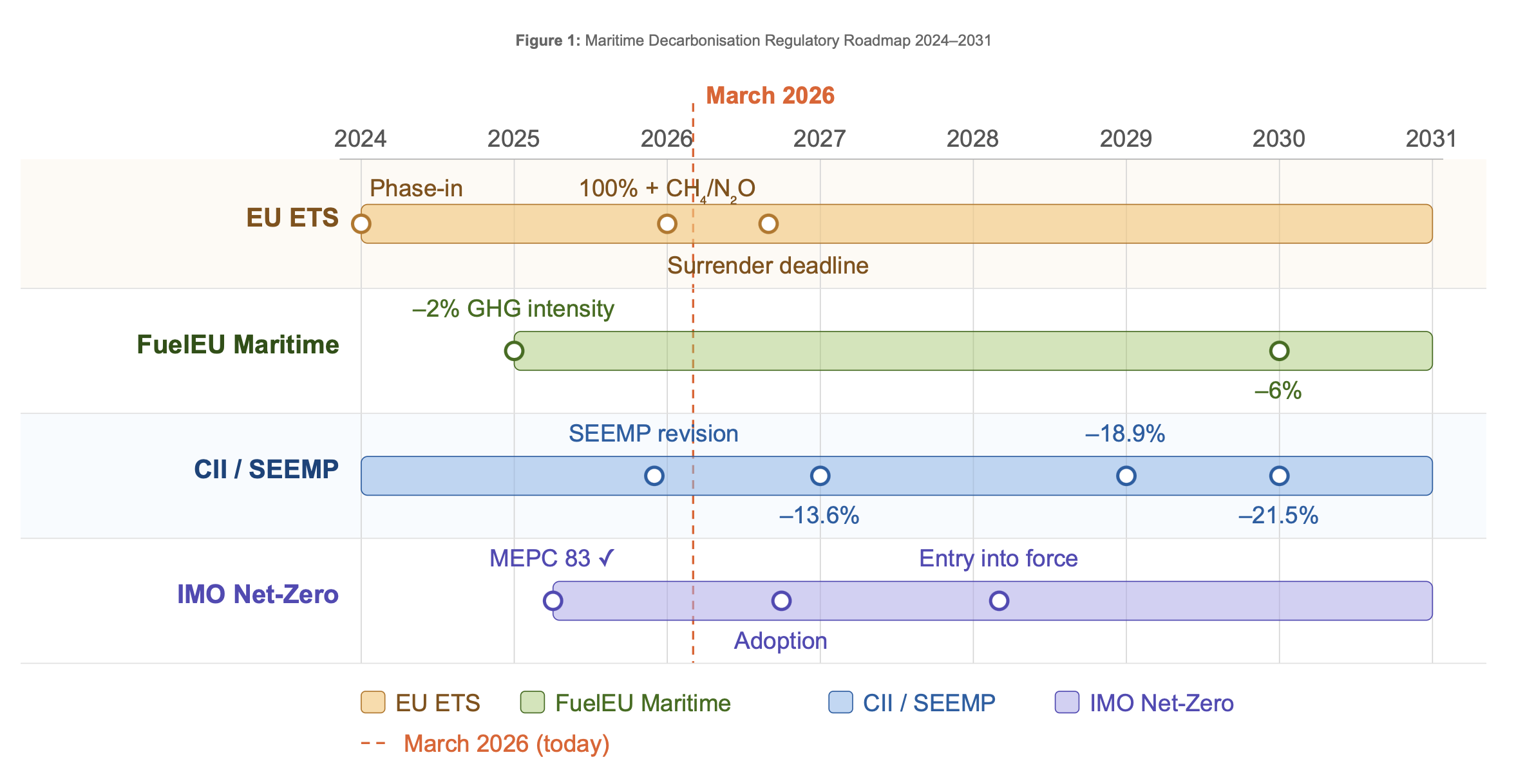

1. The Regulatory Framework: No Opt-Out Anymore

Maritime regulation has reached a tipping point. What sounded like bureaucratic future music in 2023 is operational reality in 2025, with real financial penalties and growing pressure on charter negotiations.

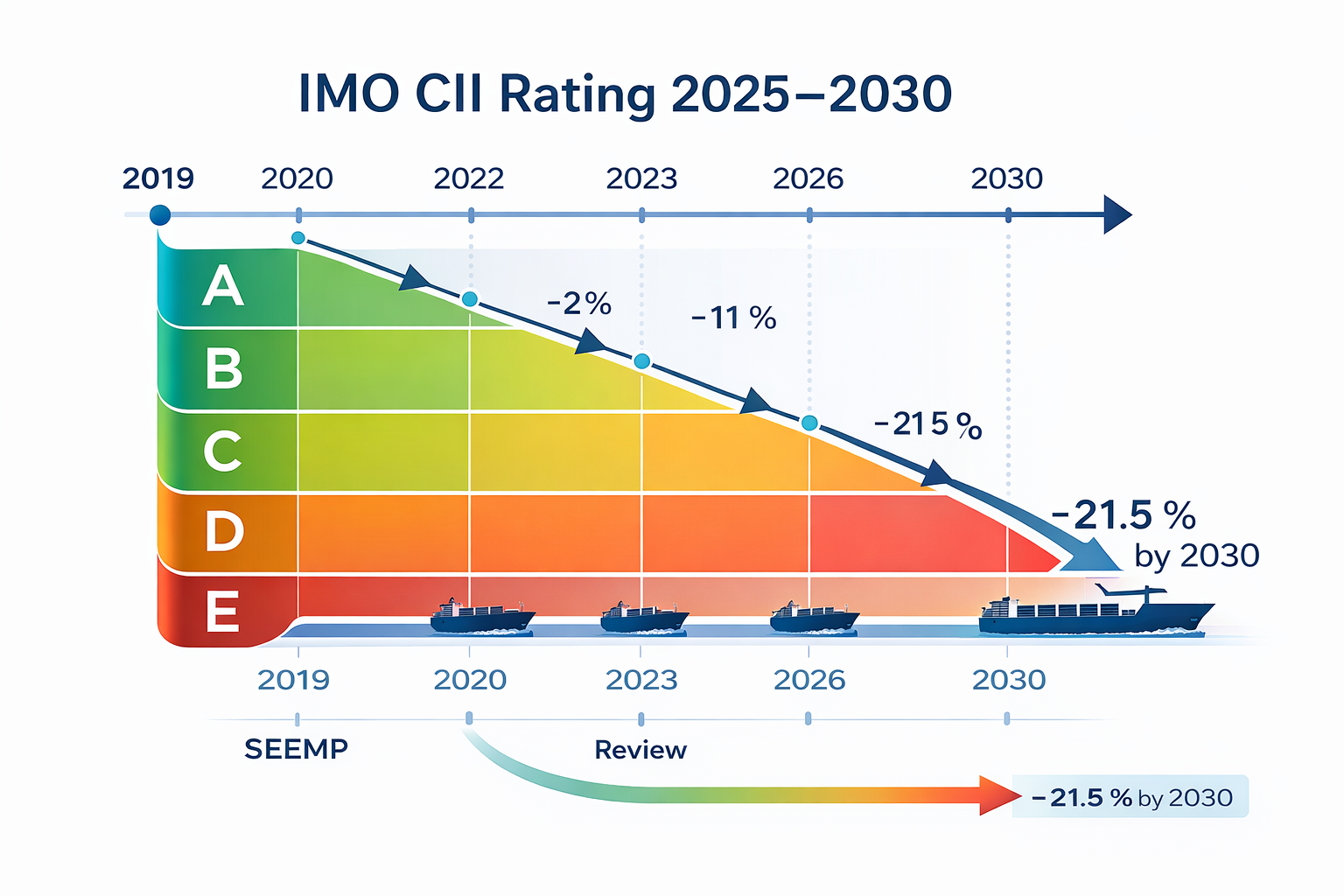

The IMO has created a three-layer compliance framework through the Energy Efficiency Existing Ship Index (EEXI), the Carbon Intensity Indicator (CII) and the Ship Energy Efficiency Management Plan (SEEMP), applicable to all vessels above 5,000 gross tonnes, effectively covering the entire international trading fleet. The CII reduction factors (Z-factors) are clearly defined: 13.625% (2027), 16.25% (2028), 18.875% (2029), and 21.5% (2030), measured against the 2019 baseline (IMO MEPC 82, 2024; IMO MEPC 83, April 2025). Ships rated D or E under CII face port access restrictions and charter value erosion, a risk now actively priced into freight negotiations.

Simultaneously, the EU Emissions Trading System (ETS) for shipping has been phasing in since 1 January 2024. From 2026, 100% of reported emissions, including methane and nitrous oxide, must be covered by EU Allowances; the surrender deadline for 2025 emissions falls in September 2026. FuelEU Maritime, applicable since 1 January 2025, sets Well-to-Wake GHG intensity limits and penalises deficits at EUR 2,400 per tonne of VLSFO equivalent, a mechanism that cannot be economically ignored.

The IMO Net-Zero Framework was approved at MEPC 83 in April 2025, with formal adoption deferred to October 2026 and earliest entry into force in March 2028. This timeline is deceptive, however: shipowners and charterers are already negotiating on the basis of these expectations. Those without an efficiency strategy in place by 2028 face not a regulatory problem but a commercial one.

👉 Key Insight: Regulation is no longer a risk scenario, it is the operating context. CII, EU ETS and FuelEU Maritime together generate financial pressure from 2026 that can be directly absorbed through efficiency measures, without waiting for the green fuels pipeline.

2. Wind Is Back, and This Time as Strategy

Rotor sails on cargo ships sound like the 19th century. They are the fastest-growing single efficiency technology in modern shipping.

Wind-Assisted Propulsion Systems (WAPS), including Flettner rotors, wing sails such as OceanWings, and kite systems, have experienced a structural breakthrough since 2024, which DNV has designated a "Breakthrough Year" for 2025/26. Over 100 ships have received installations or sit in the order book during this period; bulk carriers and tankers are leading demand. The technical logic is straightforward: rotor sails leverage the Magnus effect to convert wind energy into thrust, without fuel input, without emissions, with a scalable retrofit footprint.

Fuel savings range from 5 to 20% in isolation. In combination with voyage optimisation, weather-based routing that deliberately targets wind windows, overall savings of up to 28 to 30% are measurable (Wärtsilä Energy Saving Technology Reports, 2024–2025). 28.5% of all newbuilds now include at least one Energy Saving Device (ESD); rotor sails are the fastest-growing component within this category.

The economic case is compelling: a set of rotor sails typically pays back within four to seven years at prevailing bunker prices, while simultaneously improving CII ratings and reducing EU ETS costs. Norsepower, Anemoi Marine Technologies and Econowind are among the leading providers; early partnerships with these suppliers secure installation slots in a market where capacity for 2026/27 is increasingly booked out.

👉 Key Insight: Wind-Assisted Propulsion is no longer a niche technology. Fleets installing rotor sails or wing sails on bulk carriers and tankers today deliver the highest savings per invested euro, and structurally improve their regulatory profile at the same time.

Rotor sails on a modern bulk carrier, created using AI according to the author's specifications

3. Data Navigates: Digital Optimisation as the Quiet Efficiency Driver

No retrofit, no structural modification, yet 5 to 15% less fuel consumption. Digital voyage optimisation is the most efficient first step no shipowner should skip.

Voyage optimisation, digital twins and real-time performance monitoring are standard in new SEEMP plans as of 2025, not optional, but regulatorily expected. The methodology is clear: weather routing algorithms combine real-time oceanographic data with vessel profiles to compute the fuel-optimal course accounting for wind strength, sea state, ocean currents and port arrival windows. Savings range from 5 to 15%; when deployed synergistically with WAPS installations, an additional 12% becomes realisable (NAPA, 2025; Wärtsilä, 2024).

Digital twins do more than real-time monitoring: they model the ship as a continuous optimisation project. Hull fouling levels, propeller erosion, engine load curves, all parameters are mapped into a virtual model that delivers actionable recommendations before efficiency losses surface on the next inspection. NAPA and Wärtsilä offer lifecycle optimisation platforms that demonstrably reduce fuel consumption across a vessel's entire operational life.

The regulatory advantage is immediate: SEEMP Part III must be revised for the 2026–2028 period by the end of 2025, requiring concrete, measurable measures. A voyage optimisation platform is both the easiest and fastest-to-implement response. ROI is typically positive within six to twelve months of deployment.

👉 Key Insight: Digital optimisation is not an IT project, it is an operational lever. Anchored in SEEMP, it saves fuel, improves the CII score, and creates the data foundation for every subsequent investment decision in retrofits or alternative fuels.

4. Engines, Pumps, Auxiliary Systems: The Underestimated Efficiency Space

Engines consume 70 to 80% of a vessel's total energy. Pumps and fans account for another 10 to 20%. Together, this is the most frequently underestimated, and most rapidly accessible, efficiency pool on board.

On the engine side, the 2024–2026 trends focus on immediately realisable measures: advanced turbocharging, Miller cycle optimisation, enhanced fuel injection and friction reduction reduce specific fuel consumption by 3 to 8%. Hybrid systems combined with Waste Heat Recovery (WHR) deliver an additional 5 to 10%. Over 50% of the current order book is "alternative-fuel-ready", meaning methanol-, ammonia- or LNG-capable engines with methane slip mitigation are already installed or specified (DNV Maritime Forecast to 2050, 2025). Power limitation retrofits for EEXI compliance reduce OPEX at existing ships by up to 15%, without intervention in the underlying engine architecture.

On the systems side, DESMI OptiSave™ exemplifies a technology class that still receives insufficient attention in the market. The system optimises pumps and fans on board through automatic speed adjustment via variable frequency drives, calibrated to actual cooling demand, load profile and sea conditions. Savings on individual pump groups reach up to 90%; in practice, 250 to 350 litres of fuel per day per vessel have been measured, equating to approximately USD 42,000 per year at prevailing bunker prices (DESMI, 2025). With over 575 installations worldwide and a cumulative saving of more than 67,000 tonnes of fuel and 180,000 tonnes of CO₂, OptiSave™ is among the best-documented retrofit systems in the market.

Payback typically falls below twelve months, a figure almost no other efficiency system in maritime reaches. Frese FUELSAVE® and comparable systems complement this approach in smart valve management. The market for energy-efficient marine pumps is growing to 2033 at a CAGR of 5.2 to 5.5%, driven by CII, EEXI and FuelEU Maritime (Coherent Market Insights, 2026).

👉 Key Insight: Pumps and auxiliary systems are the most overlooked efficiency space on board, with the fastest ROI. A pump optimisation retrofit such as DESMI OptiSave™ measurably improves the CII rating, reduces EU ETS penalty exposure and typically pays back within the first operating year.

5. Combined Strategies: Where the Real Return Is

Individual measures are starting points. Combinations are strategies. Those who think rotor sails, voyage optimisation and pump management together realise savings that no alternative fuel can match at this cost structure.

The combination logic is mathematically compelling: WAPS delivers 5 to 20%. Voyage optimisation adds 5 to 15%, and amplifies WAPS effects synergistically by up to 12%, because wind windows are deliberately targeted. Engine optimisation with WHR contributes another 5 to 10%. Pump and auxiliary systems add 3 to 15%. In practice, for bulk carriers or tankers on specific routes, total savings of 25 to 30% versus the status quo are realistic and documented.

CII-Rating-Chart

The timing factor is decisive: between 2026 and 2028, regulatory pressure is at its most intense, compliance costs are rising, and early fleets will be differentiated by charter markets on the basis of CII profiles. Those implementing combined measures in this window secure competitive advantages that will materialise between 2028 and 2031, when the IMO Net-Zero Framework enters into force, in the form of lower OPEX structures and stronger market positions.

👉 Key Insight: The greatest mistake in the maritime decarbonisation debate is sequencing: efficiency first, then fuels. This logic is correct. But many shipowners are waiting for fuels before addressing efficiency. That is not strategic conservatism, it is operational negligence in a regulatory context that is already generating penalties today.

Action Recommendations

Immediate Measures, This Week

Evaluate the CII rating of all vessels above 5,000 GT against current operating profiles: who is D or E today, and which measure improves that rating fastest?

Update SEEMP Part III for 2026–2028: name concrete, measurable efficiency measures, not intentions. Voyage optimisation is the easiest entry point.

Quantify EU ETS cost exposure for 2025: use the September 2026 surrender deadline as a planning horizon; align allowance strategy with the finance team.

Initiate a pump and auxiliary system audit: which equipment runs at fixed speed despite variable demand? This is the fastest lever with the shortest ROI.

Strategic Commitments, 6 to 24 Months

Pilot Wind-Assisted Propulsion on a suitable bulk carrier or tanker: Flettner rotor systems from Norsepower or Anemoi as a starting point; run ROI calculations against current bunker prices and CII penalty scenarios.

Roll out a digital optimisation platform fleet-wide: NAPA or Wärtsilä systems with SEEMP integration; use data as the foundation for all subsequent investment decisions.

Retrofit pump management: deploy DESMI OptiSave™ or equivalent VFD systems on vessels with high cooling water demand; payback under 12 months is realistic for suitable profiles.

Define the combination strategy for 2028: which combination of efficiency and fuel measures delivers compliance with the IMO Net-Zero Framework at minimum CAPEX risk? Answer this question now, not in 2027.

Adapt charter contract strategy: explicitly address CII ratings in time charters; negotiate clauses covering efficiency improvement obligations and cost allocation for compliance gaps.

Final Thought

Shipping has a distraction problem. The debate about ammonia, green methanol and synthetic LNG matters, for 2030 and beyond. But it conceals an uncomfortable truth: 90% of the fleet operates today with technologies that are more expensive than they need to be. Efficiency is not a bridging concept. It is the foundation. Those who skip it will not only pay more, they will accumulate commercial disadvantages in a market that translates CII profiles into charter ratings, disadvantages that no subsequent fuel switch will undo. The question is not which fuel saves shipping. The question is how much of it you need if you save first.

What combination of efficiency measures has your fleet already implemented, and how significantly has your CII rating shifted over the past two years? Join the discussion or read our analysis on predictive maintenance in the maritime industry.

References

Coherent Market Insights (2026) Marine Pumps Market: Size, Share and Trends Analysis Report, 2026–2033. Available at: coherentmarketinsights.com (Accessed: March 2026).

DESMI (2025) OptiSave™ Energy Saving System: Product Documentation and Fleet Case Studies. Nørresundby: DESMI A/S.

DNV (2025) Maritime Forecast to 2050: Energy Transition Outlook. Høvik: DNV AS. Available at: dnv.com (Accessed: March 2026).

DNV (2025) FuelEU Maritime Insights: Regulatory Overview and Compliance Pathways. Høvik: DNV AS. Available at: dnv.com (Accessed: March 2026).

European Commission (2025) EU Emissions Trading System for Maritime Transport: Implementation Guidelines. Brussels: European Commission.

European Commission (2024) FuelEU Maritime Regulation (EU) 2023/1805: Technical Implementation. Brussels: European Commission.

IMO (2024) Resolution MEPC.395(82): 2024 Guidelines on the Ship Energy Efficiency Management Plan (SEEMP). London: International Maritime Organization.

IMO (2025) MEPC 83 Outcomes: GHG Fuel Intensity Standard and Net-Zero Framework Approval. London: International Maritime Organization. Available at: imo.org (Accessed: March 2026).

IMO (2025) CII Reduction Factors (Z-Factors) 2027–2030: Official Guidance. London: International Maritime Organization.

NAPA (2025) Voyage Optimization and Lifecycle Performance Management: Fleet Analytics Report. Helsinki: NAPA Group.

Research and Markets (2026) Marine Vessel Energy Efficiency Market: Global Outlook 2025–2030. Dublin: Research and Markets.

Wärtsilä (2024) Energy Saving Technologies for Shipping: Technical Performance Report 2024. Helsinki: Wärtsilä Corporation.

Wärtsilä (2025) Wind-Assisted Propulsion and Voyage Optimization: Synergy Analysis. Helsinki: Wärtsilä Corporation.